What Is Debt Collection Software? A 2026 Guide for APAC Lenders

9 Features That Separate Modern Debt Collection Software From a Spreadsheet

How Automated Payment Reminders on WhatsApp Recover More Revenue

Debt Collection Compliance in Hong Kong and Southeast Asia: The Rules That Matter

How to Choose Debt Collection Software in APAC: An 8-Point Evaluation Checklist

From Manual Chasing to Automated Recovery: A 6-Step Rollout

Debt Collection Software FAQ and Next Steps

Debt collection software is the system a lender, money lender, securities brokerage or finance team uses to track overdue accounts, automate payment reminders, record promises to pay, and move customers toward repayment across multiple channels. In 2026 the category has shifted: the best tools are no longer auto-dialers bolted onto a ledger. They are omnichannel communication and automation platforms that meet borrowers on the messaging apps they already use, while keeping every message inside the regulatory guardrails that govern lending in Hong Kong and Southeast Asia.

This matters most for the verticals where recovery is the business: licensed money lenders, consumer finance providers, securities brokerages chasing settlement shortfalls, and bank collections teams. For a money lender operating under the Hong Kong Money Lenders Ordinance, or a Singapore lender licensed by the Ministry of Law, the difference between a 70% and an 85% on-time repayment rate is not a feature checkbox. It is the margin.

This guide covers everything an operations or collections leader needs to evaluate debt collection software in 2026:

One clarification up front, because it saves wasted demos: a messaging platform like imBee is the communication and automation layer of a collections stack, not a replacement for your loan-management ledger or case-management system. It connects to those systems through integrations and handles the part borrowers actually see, the conversation. Throughout this guide we separate what messaging software does well from what a dedicated collections ledger still needs to own.

When a vendor says "debt collection software," press for these nine capabilities. The gap between a tool that has them and one that does not is the gap between automated recovery and an expensive contact list.

The table below shows why teams outgrow manual methods. A spreadsheet and a phone can collect debt. They cannot do it at scale, on time, or with the audit trail that licensed lending now demands.

| Capability | Spreadsheet + phone | Basic dialer / SMS tool | Modern omnichannel debt collection software |

|---|---|---|---|

| Reminder scheduling | Manual, easily missed | Bulk send, fixed times | Automated, triggered by loan data and behaviour |

| Channels | Calls only | One channel (SMS or voice) | WhatsApp, SMS, email, voice with fallback |

| Two-way replies | Untracked | Rarely supported | Captured, routed and logged |

| Self-service repayment | None | None | Chatbot flows for rescheduling and confirmation |

| Promise-to-pay follow-up | Memory and luck | Manual | Automatic chase on the promised date |

| Audit trail | Fragmented | Partial | Complete, timestamped, export-ready |

| Compliance controls | Person-dependent | Limited | Template approval, contact-hour rules, access control |

Note the third column. Recovering more is rarely about chasing harder. It is about chasing earlier, on the channel the borrower reads, with a process that proves itself if questioned. For a deeper look at how finance teams use messaging in practice, see our guide to 5 ways financial services teams in Hong Kong and Singapore use WhatsApp.

Across Hong Kong and Southeast Asia, WhatsApp is where customers actually read messages. An SMS may be ignored, an email may sit unopened for days, but a WhatsApp message is usually seen within minutes. For collections, where timing changes outcomes, that difference compounds across thousands of accounts. The table below compares the channels collections teams rely on.

| Channel | Typical engagement | Two-way | Rich content | Best use in collections |

|---|---|---|---|---|

| High open and reply rates | Yes, native | Buttons, documents, payment links | Primary reminders, payment arrangements, two-way support | |

| SMS | High delivery, low reply | Limited | Text only | Fallback when WhatsApp is unavailable |

| Low open rates for reminders | Slow | Rich, but easy to ignore | Formal notices and statements | |

| Voice call | Labour-intensive, low contact rate | Yes | None | High-value or late-stage accounts |

To send reminders on WhatsApp at scale, a lender uses the WhatsApp Business Platform, also called the WhatsApp Business API, WABA, or WhatsApp Cloud API. This is the enterprise version of WhatsApp, distinct from the consumer app and the small-business app. If you are unsure which account type you need, our explainer on WhatsApp Business Account types and differences breaks it down.

Three mechanics matter for collections:

Done well, this turns a one-way dunning notice into a conversation. A borrower receives a Utility reminder two days before the due date, taps a button to confirm or reschedule, and a chatbot books the new date, no agent required. Agents spend their time on the accounts that genuinely need a human, not on sending the same message 1,400 times.

Lending is one of the most heavily regulated activities in every APAC market, and debt collection sits at the sharp end of it. Two bodies of law apply at once: the lending and money-lender rules that govern licensing and borrower conduct, and the data-protection rules that govern how you use a borrower's personal data to contact them. The table maps the core regimes.

| Market | Lending / money-lender regime | Data-protection regime | What it restricts in collections |

|---|---|---|---|

| Hong Kong | Money Lenders Ordinance (Cap. 163); banks supervised by the HKMA | PDPO (Cap. 486), incl. Part VIA on direct marketing; regulated by the PCPD | Licensing and interest limits; consent for marketing use of data; reasonable contact conduct |

| Singapore | Moneylenders Act; Registry of Moneylenders under the Ministry of Law | PDPA; regulated by the PDPC | Conduct rules for licensed lenders; consent and Do-Not-Call obligations |

| Malaysia | Moneylenders Act 1951; administered by KPKT (local government ministry) | PDPA 2010; Department of Personal Data Protection | Licensing conditions; consent for processing personal data |

| Indonesia | OJK supervises licensed lending and fintech lending | UU PDP (Law No. 27/2022) | Licensing and conduct; consent and lawful basis for contact |

Hong Kong is the clearest example. The Money Lenders Ordinance (Cap. 163) governs licensing and sets a statutory cap on effective interest rates that was revised downward in a 2022 amendment. Licensed lenders also operate under conditions that shape how a borrower may be contacted. Separately, the Personal Data (Privacy) Ordinance (Cap. 486), enforced by the Office of the Privacy Commissioner for Personal Data (PCPD), governs how you use a borrower's data.

One distinction is worth internalising because it determines whether you need consent. A reminder to an existing borrower about their own overdue account is a transactional or service message, not direct marketing. But the moment you use that same channel to cross-sell a new loan or promote a top-up, you are doing direct marketing, which is regulated under Part VIA of the PDPO and requires consent. Good debt collection software lets you separate the two: Utility templates for reminders, Marketing templates (with opt-in) for offers. Blurring them is how lenders get into trouble.

In Singapore, licensed moneylenders answer to the Registry of Moneylenders under the Ministry of Law, and contact conduct is shaped by both lending rules and the PDPA, enforced by the PDPC, including Do-Not-Call provisions. In Malaysia, the Moneylenders Act 1951 is administered by KPKT, with data handled under the PDPA 2010 and its Department of Personal Data Protection. In Indonesia, the Financial Services Authority (OJK) supervises licensed and fintech lending, while UU PDP (Law No. 27/2022) sets data-protection obligations.

The common thread across all four markets: keep an auditable record of consent and every message sent, respect reasonable contact conduct, and never let a reminder system double as an unconsented marketing channel. This is also why ISO/IEC 27001 certification matters when you choose a vendor, financial regulators expect demonstrable information-security controls, not a promise.

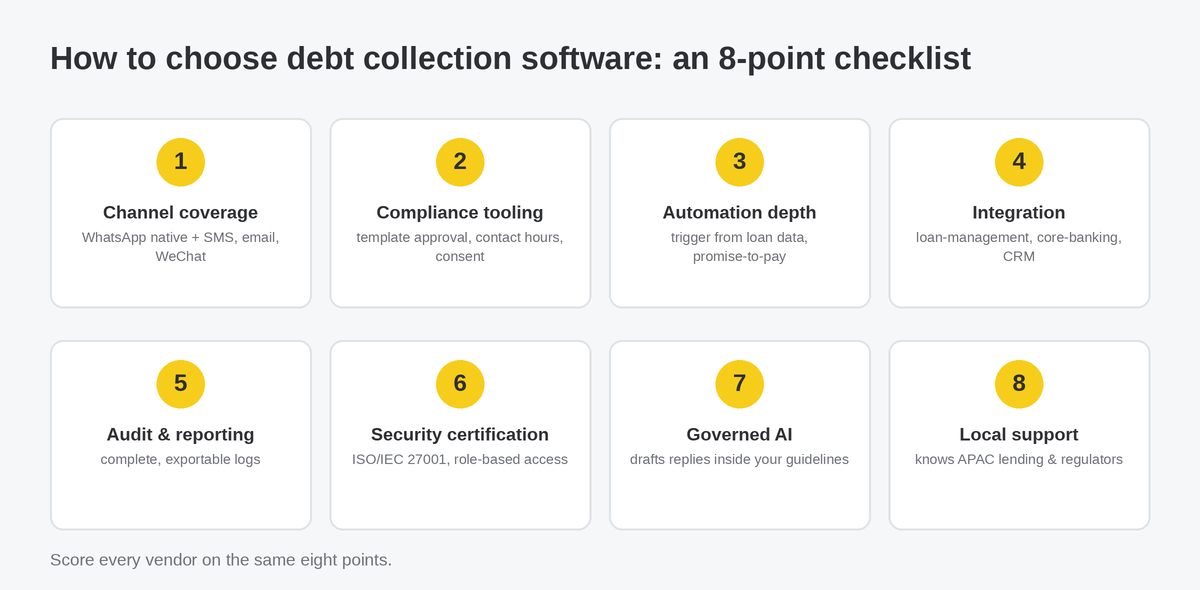

Score every vendor against these eight criteria. They are ordered roughly by how often they separate a good fit from a poor one for lenders in Hong Kong, Singapore, Malaysia and Indonesia.

Where imBee fits. imBee is an omnichannel business messaging platform, and in a collections stack it owns the communication and automation layer: a unified inbox so agents see the full history of every borrower across WhatsApp, WeChat, SMS and more; Marketing Campaign and Broadcast for scheduled, segmented reminders; Chatbot and Automation for promise-to-pay and self-service repayment flows; imBee AI for guideline-grounded reply drafting; and Data Governance backed by ISO/IEC 27001 certification. It integrates with the loan-management or collections system that holds your ledger, rather than replacing it. For a finance team, that division of labour is the point: imBee handles the conversation and the compliance of the conversation, your core system handles the money.

What imBee is not is a standalone debt-collection ledger, a payment processor or a legal-recovery case manager. If a vendor claims a single tool does all of that and the messaging too, scrutinise it, the categories solve different problems.

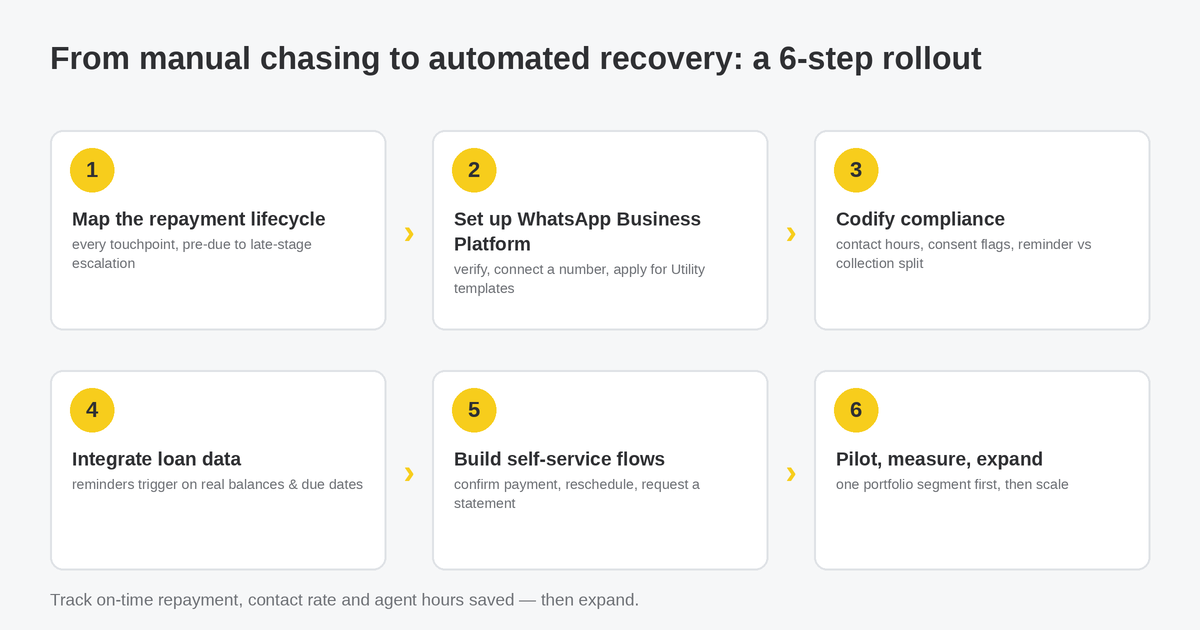

Here is the rollout that consistently works for collections and operations teams adopting debt collection software for the first time.

Two cautions. First, automate the routine, not the sensitive: hardship cases, disputes and late-stage recovery still need human judgement and often a different legal footing. Second, treat the audit trail as a feature you use, not a box you ticked, review the logs, because the same record that satisfies a regulator also shows you which messages actually recover money.

Modern debt collection software is less about chasing harder and more about chasing earlier, on the channel borrowers read, inside the rules your regulator enforces. For most APAC lenders that means a WhatsApp-first, automated, auditable communication layer sitting on top of the loan-management system that holds the ledger.

What is debt collection software?

Debt collection software is a system that automates payment reminders, tracks promises to pay, manages overdue accounts and routes borrower conversations across channels such as WhatsApp, SMS, email and voice. In 2026 the strongest platforms are omnichannel and automation-led, integrating with a lender's loan-management system rather than replacing it.

What is the best debt collection software for an APAC lender in 2026?

The best fit is a WhatsApp-first, omnichannel platform with built-in compliance controls, deep automation, broad integrations and ISO/IEC 27001 security. For the communication and automation layer specifically, imBee covers unified inbox, broadcast reminders, chatbot repayment flows and governed AI; pair it with your core loan-management system for the ledger.

Is it legal to send debt collection reminders on WhatsApp in Hong Kong?

Yes, when done correctly. Reminders about a borrower's own account are transactional messages sent via approved Utility templates on the WhatsApp Business Platform. You must respect the Personal Data (Privacy) Ordinance (Cap. 486), keep consent records, and never use the channel to cross-sell new loans without separate consent under Part VIA.

What is the difference between the WhatsApp Business API, WABA and WhatsApp Cloud API?

They refer to the same enterprise product. The WhatsApp Business Platform is the official name; WABA (WhatsApp Business Account) is your account on it; the WhatsApp Cloud API is Meta's cloud-hosted way to access it. All three are distinct from the free consumer app and the small-business app.

How does debt collection software recover more revenue?

It contacts borrowers earlier and on a channel they actually read, automates promise-to-pay follow-ups so none slip, offers self-service rescheduling that removes friction, and frees agents to focus on the accounts that need a human. The compound effect across thousands of accounts is higher on-time repayment.

Does debt collection software replace my loan-management system?

No. A messaging and automation platform such as imBee handles the borrower conversation and its compliance; your loan-management or core-banking system still owns balances, postings and the ledger. The two integrate so reminders fire on real data and a payment stops the chase instantly.

What compliance rules apply to debt collection in Singapore, Malaysia and Indonesia?

Singapore licensed moneylenders answer to the Registry of Moneylenders under the Ministry of Law, with data under the PDPA. Malaysia applies the Moneylenders Act 1951 (administered by KPKT) and the PDPA 2010. Indonesia's OJK supervises licensed and fintech lending, with UU PDP (Law No. 27/2022) governing personal data.

Why does ISO 27001 matter when choosing debt collection software?

Because you are processing sensitive financial and personal data, and financial regulators expect demonstrable security controls. ISO/IEC 27001 certification is independent evidence that a vendor manages information security to a recognised standard, not just a marketing claim.

Ready to see how a compliant, WhatsApp-first communication layer fits your collections stack? Book a demo with imBee to walk through reminder automation, repayment flows and the compliance controls above, or try imBee to get hands-on. You can also explore how financial services teams across Hong Kong and Singapore already use WhatsApp to serve customers.

Last updated 17 June 2026.

Start your 30-day free trial today. Supercharge your team's productivity by over 30% and take your business to new heights of success.